Do REITs Deserve a Place in Your Portfolio?

A practical evaluation of structure, risks, income expectations, and suitability for Indian investors.

FINANCE

Sneha Rege

2/25/20264 min read

We grow up believing one thing about wealth:

“Buy property.”

It is almost cultural. A house means stability. A second property means success. Rental income means security.

But somewhere along the way, the dream became heavy.

Heavy EMIs.

Heavy loans.

Heavy responsibility.

Heavy dependence on interest rates we cannot control.

And yet, the desire to own real estate never really left us.

That is where REITs enter the conversation.

Not as a shortcut.

Not as a hack.

But as a structure.

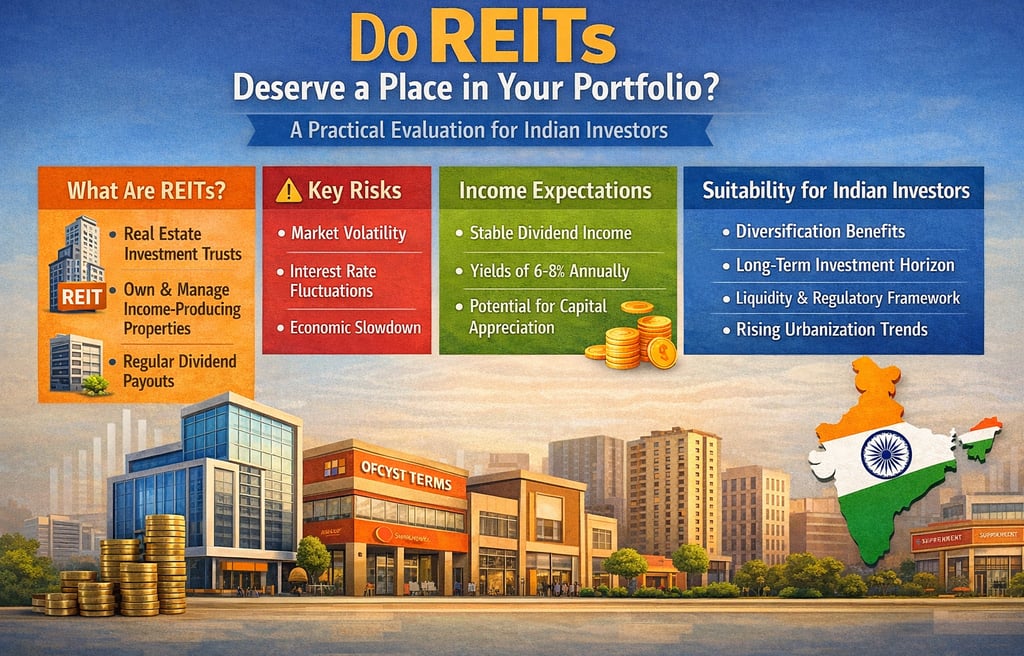

What Is a REIT?

A REIT (Real Estate Investment Trust) is like a mutual fund for real estate.

Instead of owning stocks, the trust owns physical buildings, large office parks, commercial complexes, malls.

On the other side, investors hold units, similar to shares.

So instead of needing crores to buy an office building, you can own a small piece of it.

You don’t own the keys.

You own the cash flow.

And that changes the equation.

The Two Engines of REIT Returns

REITs offer a combination of two things:

1. Regular Income (Yield)

Tenants pay rent.

After expenses, most of that cash flow is distributed to unit holders, usually quarterly.

It is structured income. Not hope-based income.

2. Growth

Just like property prices can appreciate over time, commercial buildings can increase in value.

Rent agreements usually include annual escalations. So income grows gradually too.

When you combine yield and appreciation, experts often suggest a reasonable long-term return expectation in the range of 10–12% annually.

Not magical. Not explosive. But structured.

Why This Structure Matters: The SEBI Rules

REITs in India are regulated by SEBI, the same regulator that oversees mutual funds.

And there are strict rules to protect investors:

80% Rule: At least 80% of the value must be invested in completed, rent-generating properties.

90% Rule: At least 90% of cash flows must be distributed to unit holders.

Think about that. A company is not obligated to pay you dividends.

A REIT is.

That structural difference matters.

REITs vs. Buying Physical Property

Let’s speak honestly.

If you buy residential property as an investment, what usually happens?

You take a large loan. ₹1 crore or more.

Interest rates fluctuate. Post-COVID, rates went as high as 9%. Pre-COVID, they were below 7%.

Every 0.10% matters when you are servicing a crore.

One rate cycle can lengthen your financial freedom timeline by years.

And let’s say this clearly: A person carrying a large loan is not financially free.

You may have assets. But your time still belongs to the EMI.

Now compare that with REITs:

Lower Entry Cost

You can start with a few hundred rupees per unit.

Not crores.

High Liquidity

You can sell tomorrow on the exchange.

Try selling an apartment in two days.

No Management Hassle

No repairs.

No tenant calls.

No negotiation drama.

A professional team manages it.

Lower Financing Costs

In 2025, RBI regulations allowed REITs to borrow from commercial banks, making financing cheaper. Lower borrowing costs can translate into better distributable income.

Additionally, SEBI has classified REITs as equity products. This allows more mutual funds to invest in them, increasing institutional participation and liquidity.

Structure attracts capital. And capital sustains structure.

Income: A Better Comparison

Many investors chase high-dividend stocks. They google “ Top 10 Dividend- paying stocks” and place their bets on this list.

But remember: A company is not obligated to pay dividends.

If business conditions change, dividends can stop.

And dividends are taxed at your slab rate.

REIT income typically comes in these forms:

Dividend

Interest

Repayment of HoldCo/SPV debt

Other income

Currently, for major Indian REITs, a significant portion of distributions has been non-taxable in the hands of unit holders (subject to structure and regulation).

Also, commercial rental yields are typically higher than residential rental yields.

So if income is your goal, the structure deserves attention.

But Let’s Not Romanticize It

REITs are not perfect. No asset is.

They carry risk.

Just like equity.

Just like debt.

Just like commodities.

Risks include:

Market shifts in office demand

Structural changes in how people work

Prolonged occupancy decline

Economic slowdowns

If occupancy consistently drops, review.

If rental growth stagnates structurally, review.

REITs require monitoring — not obsession — but periodic review.

Nothing in your portfolio should be on autopilot forever.

The Behavioral Angle No One Talks About

We often treat real estate as emotional.

Tangible. Safe.

But safety is not about physicality. It is about predictability.

Owning a second residential property with a floating loan is not necessarily safer than owning diversified commercial assets through a regulated trust.

In fact, concentrated leverage may increase fragility.

When you buy a house with a large loan, you are concentrated in:

One city

One property

One tenant (if rented)

One financing source

With REITs, you own exposure to multiple properties, tenants, and leases.

Diversification inside real estate.

That’s different.

REITs in Retirement Planning

In retirement planning, we often talk about the 4% withdrawal rule. Meaning: Withdraw 4% annually from your corpus to sustain income.

But what if part of your portfolio generates structured income?

What if REIT distributions cover a portion of your annual needs?

Then your withdrawal requirement from equity and debt reduces.

This is where REITs can play a role in a bucket strategy:

Growth bucket (equity)

Stability bucket (debt)

Income bucket (REITs, dividends, interest)

They may not be the hero. But they can be a strong supporting character.

A Caution Before You Jump In

If you are unsure, do not invest because of FOMO. REITs are not trending stocks.

They are regulated income-generating structures.

You need to:

Read the offer documents

Understand occupancy levels

Check lease tenures

Review debt levels

Monitor distribution history

If you do not have the time or interest, consult a fee-only planner who provides conflict-free advice.

If that is not your preference either, then stay within what you understand.

Investing without conviction creates anxiety.

And anxiety defeats the purpose.

The Bigger Question

The goal is not to replace property dreams. The goal is to question assumptions.

Do you want ownership? Or do you want income?

Do you want status? Or do you want structure?

REITs may not give you a nameplate on a gate.

But they may give you something quieter: Predictable participation in commercial real estate without leverage, without management burden, and without tying your entire freedom to an EMI cycle.

And sometimes, that quiet structure is more powerful than visible ownership.

No asset is perfect. But the right mix of imperfect assets can create stability.

REITs can be one such layer.

Not the whole portfolio. Not the entire plan.

But a thoughtful part of it.

And in investing, thoughtful usually beats dramatic.