Is Your Retirement Strategy Truly Leak-Proof?

The Three Leaks Every Retirement Corpus Has (And How to Plug Them)

FINANCE

Sneha Rege

12/14/20255 min read

You have a plan. You found the right app to track your assets. You check your net worth religiously. You think you’re on top of the investment game. But are you?

Let me give you the harsh visual reality: Your retirement corpus is a bucket full of hard-earned water, and that bucket has massive, preventable leaks.

The question isn't whether you’re saving enough. It's whether you have the expertise to make a non-biased judgment that your plan is actually right. Are you willing to risk your entire future on guesswork?

Let’s step back and identify the three biggest leaks that are secretly draining your bucket, why they’re killing your wealth, and how you can plug them before you run dry.

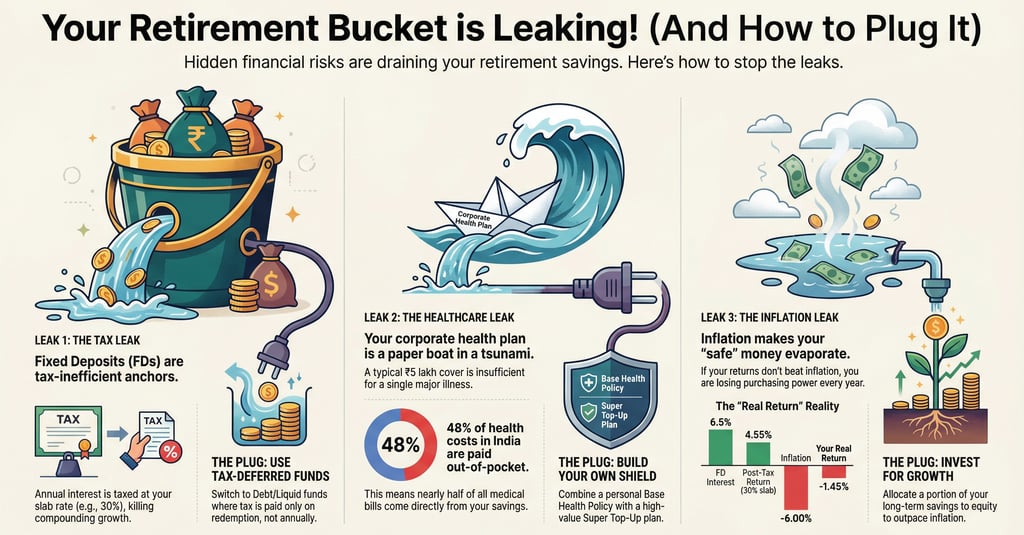

Leak 1: Tax Leakage – The Government’s Open Hose

This is the most frustrating leak. It's like having the government standing next to your bucket with a giant hose, constantly siphoning off your savings before they even get a chance to grow.

The Real-Life Drain: The FD Trap

Meet Ritesh, an IT professional in Bangalore. He earns well and saves diligently, mostly in Fixed Deposits (FDs). Every assessment year, he cribs, "It’s a sin to earn well in India! I already pay 30% taxes on my salary, and now I have to pay tax on my savings too? This is madness!"

He's right, and you’re probably nodding along. If you fall in the 30% tax bracket, you have to pay tax on the interest earned on FDs every single year, even if you just renew the deposit. They are literally tax-inefficient anchors weighing down your retirement ship.

The Simple, Brutal Calculation

Imagine you earned ₹10,000 in FD interest this year. If you fall under the 30% tax slab, you immediately lose ₹3,000 to the taxman.

That's ₹3,000 that is instantly drained from your bucket and can never compound again for the next 20 years.

The Plug: Compounding Without Annual Interruption

The rich have known this trick forever: tax deferral is your best friend.

Switch to Debt/Liquid Funds: Unlike FDs, safe mutual funds (like Liquid or Ultra Short Duration funds) don't face annual tax liability. You only pay tax when you sell (redeem).

The Power of Deferral: That ₹3,000 you saved from the taxman stays in the bucket, earning more interest for you. You get to compound the full amount, not the post-tax amount. This is a massive turbocharge over 20+ years.

The Pro Move (Satire Alert): Stop behaving like a bank manager who only believes in FDs. Move that near-term money to tax-efficient debt instruments.

Leak 2: Healthcare Leakage – The Catastrophic Hole

This leak isn't a slow drip; it's a sudden, catastrophic hole punched in the bottom of your bucket that can drain your entire corpus in weeks, forcing you back to the corporate rat race (like my colleague Sushma).

The Problem: Relying on a Paper Boat

You’re financially conscious, but like an astonishingly high number of Indians, you probably still rely on your corporate health plan. A typical corporate plan offers about ₹5 lakh cover for the entire family.

If you look at the current hospitalisation cost for a single major illness, you will realise that ₹5 lakh cover is a paper boat trying to survive a tsunami.

Real Fact (India/Global): India has one of the highest Out-of-Pocket Expenditure (OOPE) rates globally, hovering around 48% of total health spending. This means nearly half of medical costs come directly from your savings, not insurance.

The Cost Shock: A standard angioplasty in a major metro hospital costs ₹3–5 lakhs. A full cancer treatment course can easily exceed ₹20–30 lakhs. Your corporate cover might not last a single week in the ICU.

The Real-Life Drain

Imagine you’ve diligently built a corpus of ₹25 lakhs. One not-so-fine day, you are diagnosed with a critical illness. Your ₹5 lakh corporate cover is exhausted in two weeks. Now, you are forced to dip into your ₹25 lakh corpus. What if the market is doing poorly that month? You are forced to redeem equity at a loss just to pay bills.

This leak is enough to instantly drain whatever you built with hard work and consistency. A single health event can wipe out 5-10 years of consistent saving and compounding.

The Plug: Your Own Shield (Base + Top-Up)

You need a strong, personal shield that stays with you forever.

Opt for Personal Base Cover: Immediately purchase your own personal health insurance policy. This policy follows you, not your job.

Use Top-Up Plans: For serious protection, combine a manageable base cover (e.g., ₹10 lakh) with a Super Top-Up plan (e.g., ₹50 lakh). These are surprisingly affordable and give you massive protection against major events without breaking the bank on premiums.

The Critical Timing: Increase your cover as you close in on early retirement. Getting a high cover before you leave full-time employment is vital, as increasing it later when you have pre-existing conditions or no fixed salary is difficult and expensive.

Leak 3: Inflation Leakage – The Invisible Evaporation

You see colleagues boasting about their ₹30 lakh FDs. Once upon a time, you might have envied them. But as financial awareness grows, you realise that boast is actually a warning sign: their money is evaporating.

This leak is slow, silent, and invisible. It doesn't reduce the number in your bank account, but it constantly reduces the purchasing power of the water in your bucket.

The Problem: The Negative Real Return

The Government might quote a general CPI of around 5-6%, but the sad reality is that your two most important expenses run much higher: Education (10–12%) and Healthcare (12–15%).

If you rely solely on safe, low-return products, you're guaranteed to lose.

Let’s combine Leak 1 and Leak 3 for the ultimate horror show, the Tax-Inflation Double Impact:

FD Interest: 6.5%

Tax Leak (30%): -1.95%

Post-Tax Return: 4.55%

General Inflation Leak: -6.00%

Your Real Return: -1.45%

You are losing 1.45% of your purchasing power every single year! This is the brutal math behind the saying: If inflation averages 6%, your money loses 50% of its value in just 12 years.

The Plug: Balancing Safety and Growth (The Equity Lever)

The only way to stop the evaporation leak is to generate returns that are higher than your expense inflation rate. This requires accepting a calculated, not blind, risk.

The Growth Leg (Equity): Your main retirement corpus needs one leg firmly planted in diversified, well-researched equity products. Historically, Indian equity markets have delivered 12-15% over the long term, which is the only asset class proven to beat that cruel healthcare and education inflation.

The Safety Leg (Debt): Keep your other leg in safe products like high-quality debt funds or FDs only for your near-term cash needs (3-5 years). This money is there to stay safe, not to grow big.

Conclusion: Stop Guessing, Start Plugging

Your retirement bucket is not invincible. The three leaks: Taxation, Healthcare, and Inflation, are constantly at work, often without you noticing.

You can't afford to lose money to the Tax Leak (FDs).

You can't afford to have your corpus wiped out by the Healthcare Leak (No Personal Cover).

You can't afford to have your savings evaporate due to the Inflation Leak (No Inflation Beating Growth Engine).

The biggest challenge in retirement planning is making a non-biased judgment on your strategy. Most people are using the same leaky bucket their parents did. That old playbook is a recipe for disaster.

Stop using hope as a strategy. Start designing your escape plan with plugs: Use tax-efficient funds, secure high personal health cover, and introduce equity growth at an allocation that works for you to beat inflation.

Are you willing to audit your bucket right now and see where your biggest leak is?