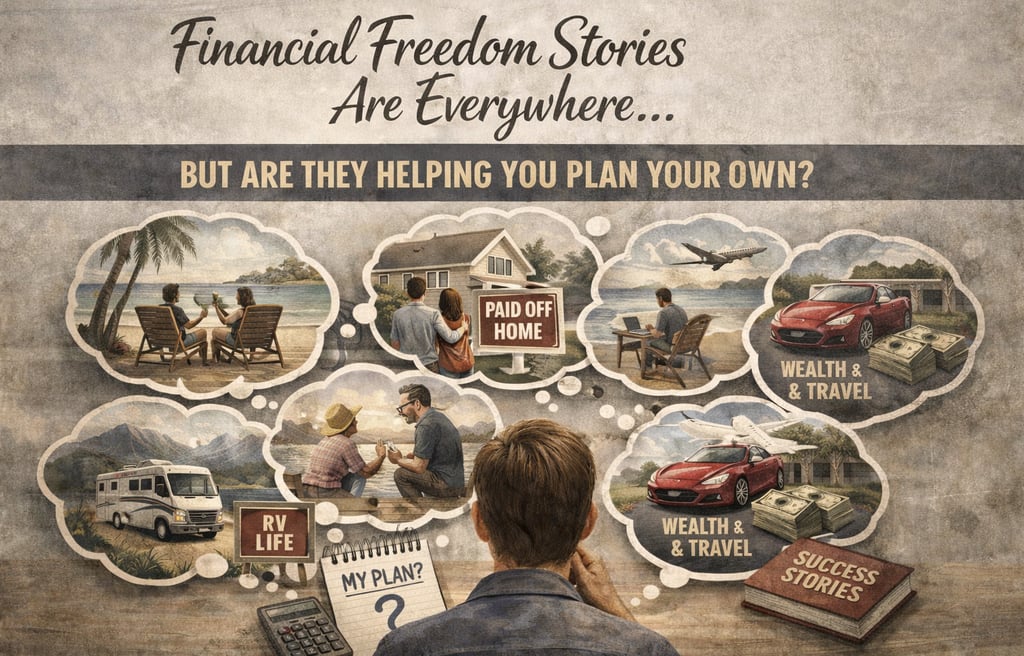

Financial Freedom Stories Are Everywhere. But Are They Helping You Plan Your Own?

Sneha Rege

1/18/20265 min read

Every week, a new financial freedom story shows up on YouTube.

A new video.

A new podcast.

A new educator who has “achieved financial freedom” and now wants to teach others how to do the same.

Platforms like Wint, Upsurge, INDmoney, Groww are full of such stories, many with lakhs of views. And that tells us one thing very clearly:

No matter how common the theme becomes, we still want to know:

How did this person escape the corporate prison? What numbers did they reach? What exactly did they do?

The curiosity is natural. I click too.

The Temptation of the Perfect Exit Story

More than half of these stories follow a familiar pattern.

Someone quits the corporate race

Moves from a “polluted city” to mountains or beaches

Talks about raising kids in fresh air (as if the rest of us don’t care about that)

Shows a life of travel, slow mornings, and freedom

The thumbnails are irresistible.

“Retired at 40.”

“Left corporate forever.”

“Escaped the rat race.”

You click hoping—this time—you’ll finally find something practical.

Some insight you can apply.

Some framework that fits your own life.

But what we usually get instead is… another outlier.

The Problem With Outliers (And No, This Is Not Jealousy)

Let me be clear:

I am not here to discredit anyone’s success.

What would I even gain from that?

The people featured in these stories worked hard. They took risks. They were disciplined. Hats off to them.

But crediting a repeatable strategy to a story that is built on non-repeatable advantages is where things go wrong.

Let’s look at a few examples.

Aman Upadhyay retired with a ₹10+ crore corpus and now teaches financial education.

His outlier? Senior executive roles and a US stint that fast-tracked wealth creation.Neeraj Arora achieved a ₹34+ crore corpus, is financially independent, and still teaches CA and personal finance.

His outlier? Parents who were financially literate and invested early in equity, giving him a massive head start.Sanjay Kathuria built a ₹10+ crore corpus.

(Again—career trajectory, timing, and opportunities that most salaried people won’t replicate.)One early retiree featured on Groww openly mentioned inheriting substantial real estate.

Another story on INDmoney involved ESOP wealth from a startup exit—again, timing and access mattered.

The list goes on.

These are not “wrong” stories.

They are just not typical.

The Silent Majority No One Talks About

So here’s the real question I struggle with:

What about the common salaried individual earning ₹50,000 to ₹1 lakh a month?

No entrepreneurial ambitions.

No foreign stint.

No inheritance.

No startup lottery.

And working in an increasingly uncertain IT and corporate market.

Does that mean early retirement is not for them?

Does it mean anything below ₹8–10 crore is “not good enough”?

Does it mean financial freedom is only for a privileged few?

Unfortunately, the way these stories are presented often skews reality.

People walk away believing:

They must accumulate ₹8–10 crore

They must invest ₹1 lakh SIP every month

They must leave cities, buy land, start cafés or homestays

Or worse—quit jobs and sell expensive “financial freedom” courses after a US stint

None of this is mandatory. None of it is universal.

Before Asking “How”, Ask “Why”

Early retirement planning starts at the wrong place for most people.

Not with why, but with how much.

Before debating:

25X vs 30X

3% vs 4% withdrawal

FIRE vs Lean FIRE vs Fat FIRE

Ask yourself:

Why do I want to retire early?

Am I unhappy with work—or just burnt out?

Is my workplace toxic, or do I need a role change?

Do I regret my line of work?

Can I reduce stress without quitting entirely?

Clarity on why changes everything.

The Only Math That Actually Matters Early On

Once your why is clear, then comes the how much, and this is where simplicity beats sophistication.

Start with:

Essential expenses: costs that will exist even after you exit corporate life

Lifestyle expenses: comforts you value

Discretionary expenses: upgrades, gadgets, travel

This clarity does two things

Grounds your retirement number in reality

Forces you to think about supplementing income post-retirement, not fantasizing about doing nothing forever

Most people won’t sip Mai Tais on a beach for 40 years. And that’s okay.

What Are You Really Optimizing For?

Everyone’s answer will be different.

Want a large corpus? Continue working longer.

Want mental health? Secure essentials first, not lifestyle upgrades.

Want to explore purpose or passion? Build a safety net, then take the leap.

There is no moral superiority in any choice.

As long as your basic survival is secured, you are free to pursue whatever the hell you want.

As Gen Z says—YOLO.

There Is No One Number. But There Is a Framework.

Early retirement is not a destination with a fixed price tag.

What is common across all sensible plans is the framework:

Find YOUR why?

Find YOUR how much?

Find YOUR when?

That’s it.

No clickbait.

No envy.

No borrowed dreams.

Just honest planning, rooted in your life.

If you are planning early retirement and feel overwhelmed by numbers you see online, pause. The problem may not be your savings rate, it may be the stories you are comparing yourself to.

So What Does a Realistic Retirement Framework Look Like?

Once you strip away the noise, retirement planning is not a secret formula.

It is a structured thinking process, repeated honestly over time.

Let’s extend the framework.

1.Finding Your Why (Not the Instagram Version)

Early retirement is often sold as:

No alarm clocks

Endless travel

Complete freedom

In reality, most people want early retirement because of one or more of these:

Chronic burnout

Loss of meaning at work

Health concerns

Desire for flexibility, not idleness

Fear of being stuck in a job they can’t physically or mentally continue till 60

Example:

A 42-year-old IT professional doesn’t hate working but hates the constant pressure, late calls, and fear of layoffs. Their why is not “never work again”, but “regain control over time”.

This clarity changes everything:

They may aim for Lean FIRE or Coast FIRE

They may continue part-time or low-stress work later

Their corpus need drops significantly

2. Finding How Much (Without Getting Paralyzed by Math)

This is where most people overcomplicate things.

Instead of starting with:

25X / 30X / 35X

3% vs 4% withdrawal debates

Start with expenses.

Break expenses into three buckets:

A. Essential expenses

These don’t disappear after retirement:

Food

Utilities

Healthcare

Basic housing

Insurance

B. Lifestyle expenses

Comforts you choose to keep and be flexible with:

Eating out

Domestic travel

Help at home

Subscriptions

C. Discretionary expenses

Nice-to-haves:

Phone upgrades

Luxury travel

Branded shopping

Example:

A household spends ₹1 lakh a month today.

Essentials: ₹60,000

Lifestyle: ₹25,000

Discretionary: ₹15,000

If their goal is freedom from stress, not luxury, they may plan retirement around ₹60–70k/month, not ₹1 lakh.

That single decision can reduce the required corpus by crores.

3. Understanding FIRE Is a Spectrum, Not a Badge

FIRE is not binary. You don’t either “have it” or “don’t”.

Common variants (simplified):

Lean FIRE – Essentials covered, lifestyle modest

Regular FIRE – Comfortable life, fewer compromises

Coast FIRE – Enough invested; no need to save aggressively anymore

Example:

A 45-year-old couple with ₹2.5 crore invested may:

Cover essentials through corpus

Supplement lifestyle expenses through teaching, freelancing, consulting

They are not “retired” by YouTube standards, but they are free.

4. Finding When (The Most Ignored Question)

Most stories jump from how much straight to I quit.

But when matters just as much.

When will kids’ education peak?

When will healthcare costs rise?

When does job risk increase?

When does energy decline?

Example:

Someone plans to exit corporate at 48, not 38, because:

Kids’ education costs reduce after 45

Home loan ends by 46

Peak earnings are between 40–48

That decision alone can make the plan far more robust.

5. Retirement Is Not “No Income Forever”

This is the most damaging myth.

Most people will:

Earn something post-retirement

Teach, consult, freelance, write, or advise

Choose lower stress over zero work

Planning for some income:

Reduces pressure on the corpus

Increases longevity of savings

Improves mental health

Example:

If a household needs ₹70,000/month and earns even ₹25,000 post-retirement, the corpus only needs to support ₹45,000.

That’s a very different plan from “I need 10 crore”.

6. What Real Retirement Planning Actually Looks Like

In real life, planning looks like this:

Revisit expenses every year

Adjust expectations with life changes

Accept uncertainty instead of fighting it

Build buffers instead of perfect forecasts

It is boring.

It is iterative.

It is deeply personal.

And that’s why it works.

Final Thoughts

Financial freedom is not about escaping work.

It is about escaping fear.

Fear of:

Toxic jobs

Uncertain health

Financial helplessness

Being stuck without options

You don’t need an outlier story to fix that.

You need clarity, honesty, and a framework that fits your life.

And that, quietly, is enough.